ASML Holding - pick-and-shovel play of Semiconductor Industry

ASML Holding - pick-and-shovel play of Semiconductor Industry

Investment Thesis

ASML is pick-and-shovel play of the Semiconductor industry as it provides machines to manufacture chips. Key customers are TSMC, Intel, Global Foundry, SK Hynix, Samsung, etc.

This is one of the highest-quality business, supported by Innovation and R&D.

Even though ASML supply machines for cyclical industry, there’s secular tail-wind for the Semiconductor chips (processors graphics chips, memory), used by Data Center, Autonomous Vehicle, Artificial Intelligence, Smartphones, 5G devices, IoT, etc.

On going transformation of the digital infrastructure, along with the secular end market drivers, such as 5G, AI and high-power compute, will continue to fuel demand for advanced process nodes, both in Logic and Memory, which drives the demand for ASML products, specifically for EUV lithography systems.

Qualitative

ASML makes lithography systems for the semiconductor industry. Lithography systems are required for all semiconductor manufacturing.

Photolithography technology - process by which microscopic circuits are etched onto wafers that ultimately become individual chips. It consists of shining light (UV) through different "masks" (design template) in a layered fashion to harden the systems design into the wafer. Currently, this is the only method to make semiconductor chips of all types.

Moat - ASML has

monopolyin extreme ultraviolet lithography (EUV) systems, which is required to make the most advanced 7nm and lower nodes chips. Lower nodes allow more transistors on chips, which increases its processing power. As all advanced semiconductor chips are moving towards 7nm and lower nodes chips, it will help to boost ASML market share vs. competition (Nikon, Canon, Applied Materials and LAM Research).ASML has almost 2 decades (20 years) long lead on EUV lithography as compared to competitions. Started working on EUV around 2000 and only able to mass produce chips on EUV until 2018-2019.

ASML shipped 18 EUV systems in 2018 and 26 systems in 2019. Management provided the guidance of 45-50 system capacity for 2020. Also, Management is expecting 20% growth in EUV systems revenue for 2021.

Logic EUV capacity - 1 EUV layer required 1 EUV system for every 45k wafer starts per month

DRAM EUV capacity - 1 EUV layer required 1.5 to 2 EUV system for every 100k wafer starts per month

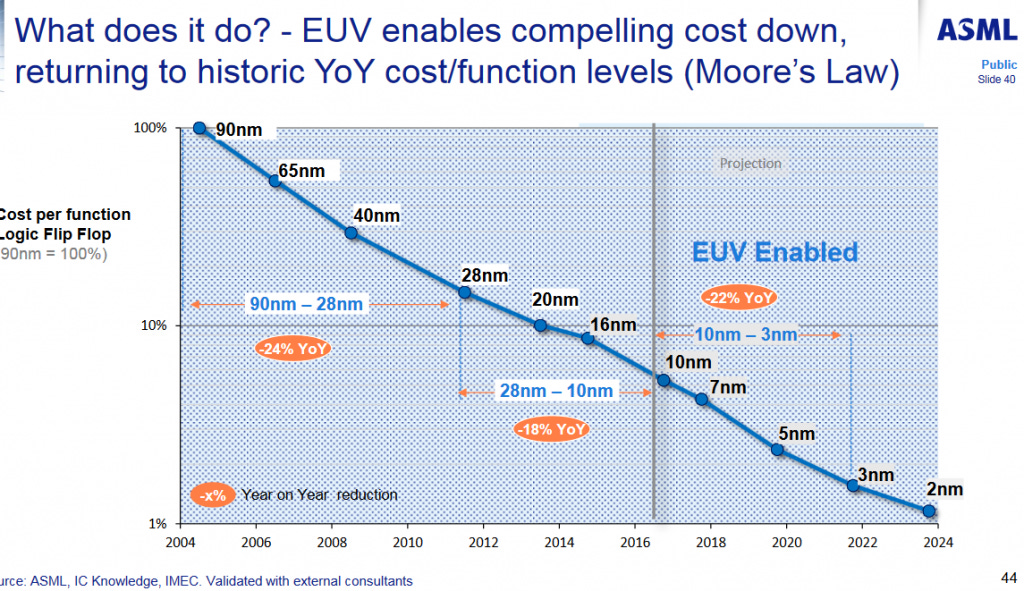

ASML is expecting EUV value increase and cost reduction to bring EUV gross margin to comparable level us DUV by 2025.

Value for customers using ASML EUV Lithography

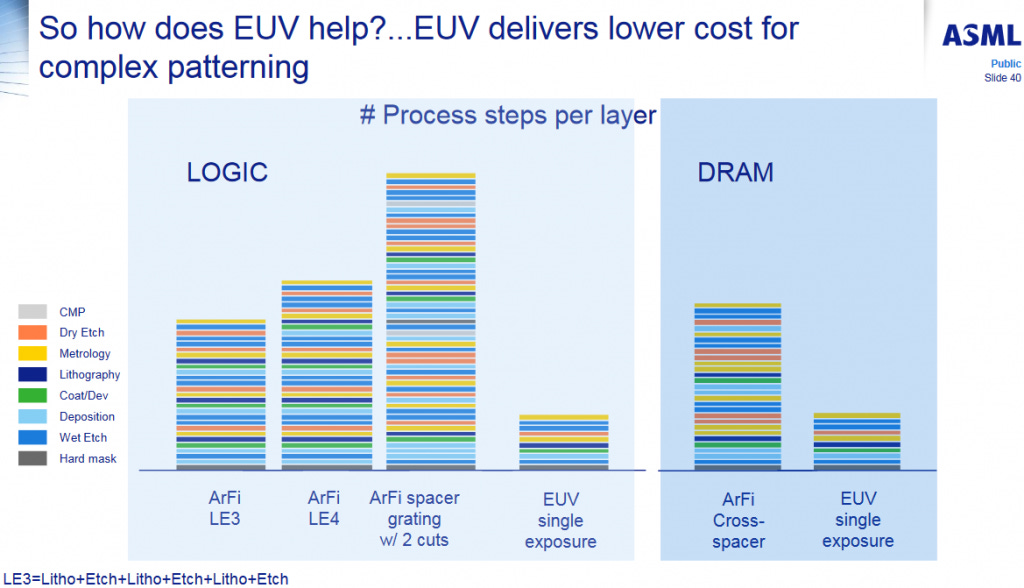

EUV simplifies process complexity to enable customers to drive cost effective patterning scaling beyond 7nm Logic and 16nm DRM

15 to 50% cost reduction as compared to multi-patterning schemes

3x to 6x cycle time reduction compared to critical multi-patterning layers

Quantitative

According to The Information Network's report, Applied Materials, which had a market share of 19.2% in 2018 (which was down from 23.0% in 2015), will increase its share of the total market slightly to 19.4% in 2019. However, ASML, which held an 18.0% share in 2018, will jump to a 21.6% share in 2019, becoming number one in market share.

According to market research firm Market Insights, the EUV lithography market is expected to grow at a 26.4% annual pace from 2019 to 2026 — with all that benefit going to ASML.

EUV system costs around $120 million vs traditional deep ultraviolet lithography (DUV) costs only one-third of EUV systems. ASML monopoly position in EUV systems, gross margin is already reaching 47%, and expected to reach 50% by 4Q20.

EUV system revenue is continuously increasing and first time surpassed DUV (deep UV) system revenue. In 3Q20, EUV system revenue was 66% of total system revenue. Also, for the end-use segment, Logic segment has increased from 45% in 2018 to 75% in 2020 whereas Memory segment is only 25%.

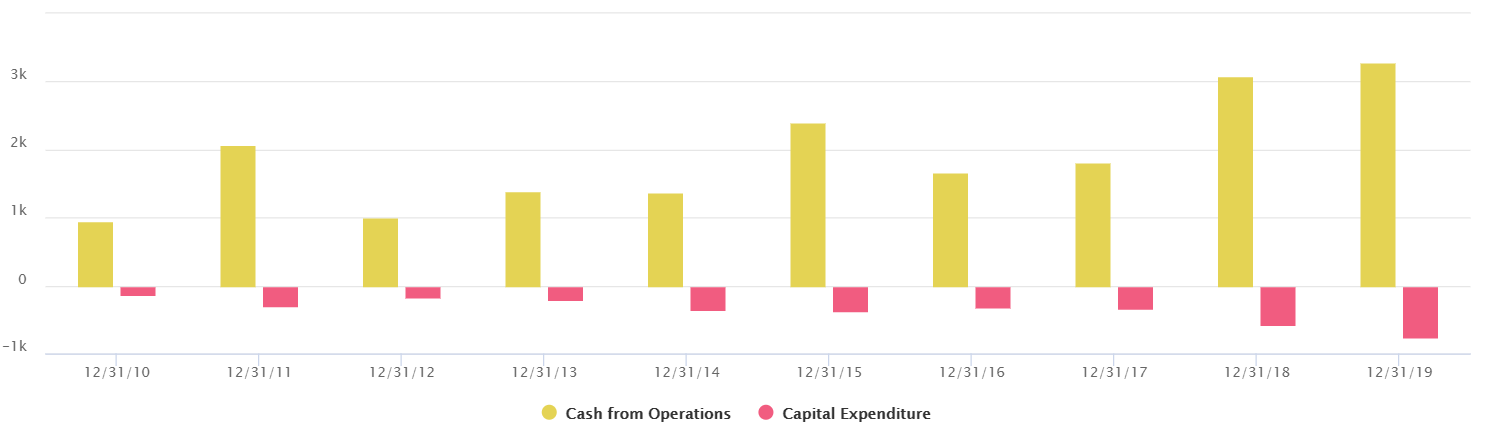

Financially strong and robust company - FCF is constantly increasing from $2.0bn in 2015 to $2.6bn in LTM. Also, company got $4.4bn in cash & cash equivalents and short-term investments to pay for the long-term debt, which is also ~$4.6bn as of LTM. Net sales has doubled since 2015 and gross margin is pretty healthy at 47%, projected to increase to 50% by 4Q20 driven by higher immersion volume and improved deep UV product mix.

ASML current LTM (as of 3Q20) revenue is $13.7bn. At a growth rate of 20% for next 5 years, projected revenue will be $34bn by 2025. With net margin 27%, earnings will be $9.2bn. At PE multiple of 50, we are looking at market capitalization of $460bn, which is 2.3x from current market cap of $202bn. CAGR of 18% for next 5 years.

Risks

ASML growth largely depends on more & more semiconductor chips moving to 7nm technology node or lower technology node. However, for many chips, lower price is more important than density, power or efficiency, so they will stay at higher technology node, like 20nm or higher. However, Industry will eventually move to lower node technology to support more transistors in given space and will drive the EUV systems growth. For example, chips used for AI, high-end PCs, Autonomous Vehicle, etc. will all demand for 7nm technology node or lower.

ASML may lose its monopoly in EUV technology. Nikon and Canon are the closest competitors in this space, however they are at least decade away in commercializing EUV technology.

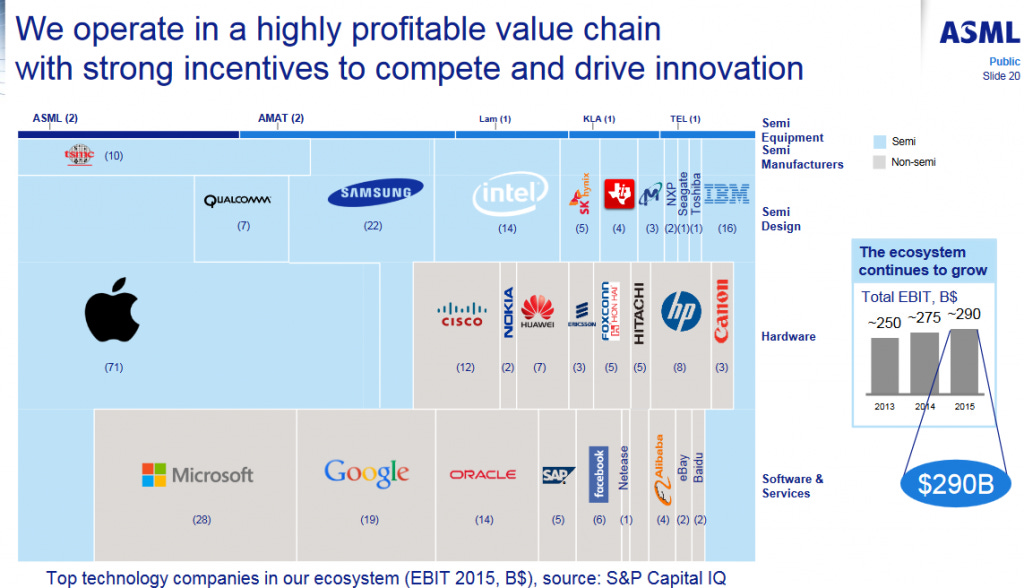

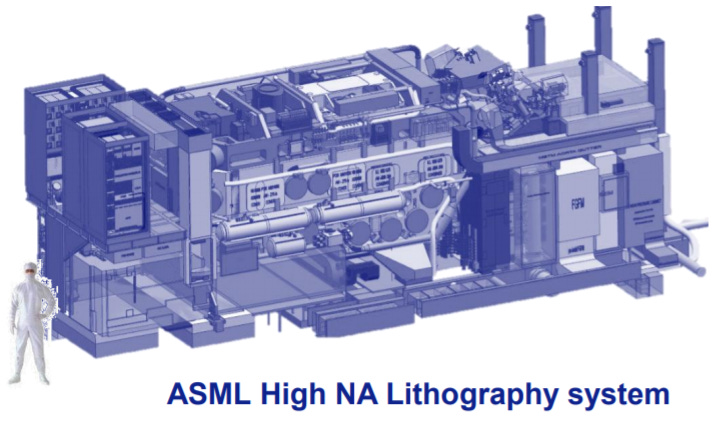

Few slides from ASML investors presentation -